Custom Car Insurance: How to Properly Insure a Modified or Built-From-Scratch Vehicle

Intro

Maybe you’re thinking of dropping a supercharger in your C7 Stingray. Or adding power brakes and a 5-speed to your C3.

Or perhaps you’re thinking of building a Factory Five Mk4 roadster in your garage as a retirement project.

In all three cases, you might be wondering: how am I going to insure this thing?

We’re here to tell you that insuring a modified or custom car isn’t just possible – it may be easier (and cheaper) than you think.

But there are definitely ways to do it wrong. So let’s cover custom car insurance: how it works, expensive mistakes to avoid, and how to get the best bang for your buck.

What qualifies as a modified or custom vehicle?

First things first, what’s the difference between a modified and custom vehicle?

- Modified vehicles are factory-made vehicles fitted with non-factory parts. A C8 Stingray with a ProCharger supercharger – or a C3 with a lightweight acrylic T-Top – are both examples of modified vehicles.

At NCM Insurance we consider a vehicle to be “modified” when the performance has been increased 25% or more, the body, chassis, or frame have been altered, a custom paint job over $10K in value, more than $5,000 in other modifications, or a stereo over $3,000. - Custom vehicles are built almost entirely from scratch. The 1961 Mako Shark Corvette, 1966 Batmobile and the infamous Oscar Meyer Weinermobile are all classic examples of custom vehicles. A “kit car” that you build in your garage – like the RCR Superlite-SLC – might also be considered a custom car.

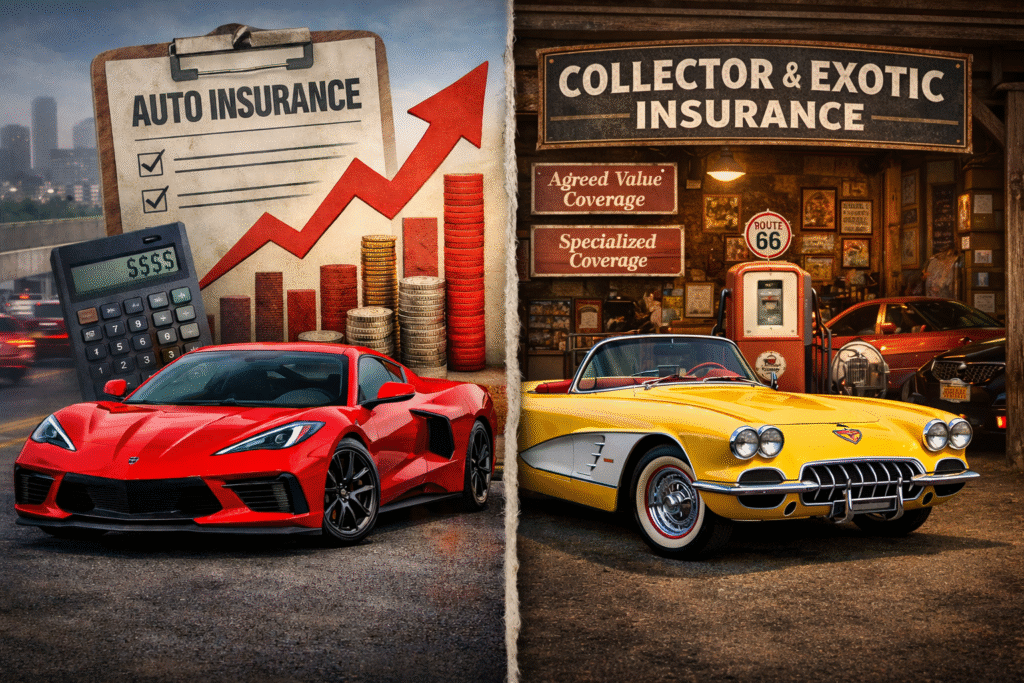

Why standard auto insurance fails modified and custom vehicles

If you’re dedicated enough to own a custom or modified car, chances are that you’ll want it properly insured, too.

But this is where many traditional insurance providers fall flat.

Let’s say you purchase a C6 Corvette for $30,000 and install an A&A supercharger for $10,000. Then, you call a traditional insurance provider for a quote.

From there, a traditional provider may do one of four things:

- Decline coverage. Traditional providers may refuse to cover custom or modified vehicles for a litany of reasons. They may be unable to properly assess their value, view them as high-risk, etc.

- Insure it for the non-modified value only. Conversely, a traditional provider may write you a policy without protecting your expensive mods, leaving massive gaps in coverage.

- Charge elevated premiums. On top of already-high premiums for sports cars, traditional providers may require you to purchase supplemental insurance to cover your modifications.

- Deny claims and cancel your policy. Finally, if you’re already insured and you disclose your mods to your provider, they’ll sometimes cancel your policy outright. And if they discover undisclosed modifications during a covered repair, they may instantly deny your claim.

How to insure a modified or custom vehicle

Rather than strong-arming a traditional provider who doesn’t really want your business, the best way to purchase custom car insurance is through a specialty insurance provider that can offer superior coverage for better value.

Here’s what the process of purchasing custom car insurance looks like:

- Find the right specialty insurance provider. When searching for the right provider to insure your custom or modified vehicle, it helps to be specific. If you have a Ford Street Rod, search “Ford Street Rod insurance.” This will help you connect with a provider – and a team of specialists – who truly understand your vehicle’s value and needs.

- Determine the Agreed Value of your vehicle. With Agreed Value coverage, you and your provider will have an honest, amicable discussion and shake hands on the car’s value upfront – factoring in things like rarity, modifications and more. That way, you’ll know what your payout amount will be in the event of a total loss.

- Update and adjust your policy as needed. Car modifications are like tattoos; once you get one, it’s hard to stop. If you do plan to modify your vehicle further, it’s wise to let your specialty insurance provider know in advance so you can discuss a new Agreed Value and factor new premiums into your project budget.

How modifications impact coverage and claims

If you are considering dropping a $10,000 supercharger in your C6 Corvette – or getting a patriotic paint job on your C3 – how would such a big modification affect your insurance situation?

With traditional insurance, modifying your vehicle to the tune of $2,000 or more (pun intended) can lead to coverage gaps, claim denials and policy cancellations.

With specialty insurance, however, modifying your car is typically much less punishing than that. As a direct result of declaring mods, you may see three concrete changes to your custom car insurance policy.

- Increased premiums. An increase to your Agreed Value will generally lead to a small increase in premiums.

- Increased claim payouts. If your modifications lead to a higher Agreed Value, you’ll receive a larger payout in the event of a total loss.

- Longer lead times for covered repairs. Naturally, it’ll take longer to repair a modified vehicle than a bone stock one. But a good specialty provider can connect you with the right parts and labor to return your vehicle to pre-loss condition.

Insuring custom builds vs. factory vehicles

As for insuring a custom-built car, any vehicle built from the ground up will be much more difficult to repair or replace than a bone-stock factory equivalent.

As a result, the owner of the Mako Shark may see two key differences in his insurance situation than the owner of a regular C3:

- Higher likelihood of a total loss. Since it may be impossible to repair or replace a one-off custom car, the likelihood of it being “totaled” following an accident goes up.

- Higher premiums. Since your custom car has a higher chance of being totaled, your premiums will likely be much higher to compensate.

Even still, “higher” doesn’t have to mean “high.” At NCM Insurance, we understand that owners of highly modified cars tend to drive less (and less aggressively) in order to preserve the value of their special vehicle.

Protect the time, money, and craftsmanship in your custom car. Request a custom

{kind=link}